Tencent Holdings - China's digital goliath

For use by institutional investors only. Not for use with the general public.

Key takeaways

- Tencent has a direct link to 1.4bn consumers via its Weixin (WeChat) ‘super app’

- Supported by powerful network effects, the company has prominent positions in multiple large markets with strong growth tailwinds

- AI integration is gathering pace across the Tencent ecosystem, with the potential to deepen its competitive moat

In 7 Powers, his influential study of enduring competitive advantage, Hamilton Helmer identifies network effects as one of the most powerful drivers of long-term business success. A company “where the value realized by a customer increases as the userbase increases,” Helmer argues, benefits from a self-reinforcing dynamic – one that fuels growth, inhibits competition, and builds market share.

In the West, Meta is perhaps the archetypal network effect success story; originally via Facebook and now increasingly through Instagram and WhatsApp. Microsoft and Visa are other high-profile examples. In China, Meta’s nearest analogue is Tencent Holdings; a digital goliath servicing some 80% of the population.

A brief survey of Tencent’s market positions illustrates both the company’s breadth and depth:

- The largest video gaming company in the world

- One of largest online advertising companies in China

- The leading domestic video and music streaming platform

- One of two dominant consumer payment wallets in China

- China’s third largest cloud provider

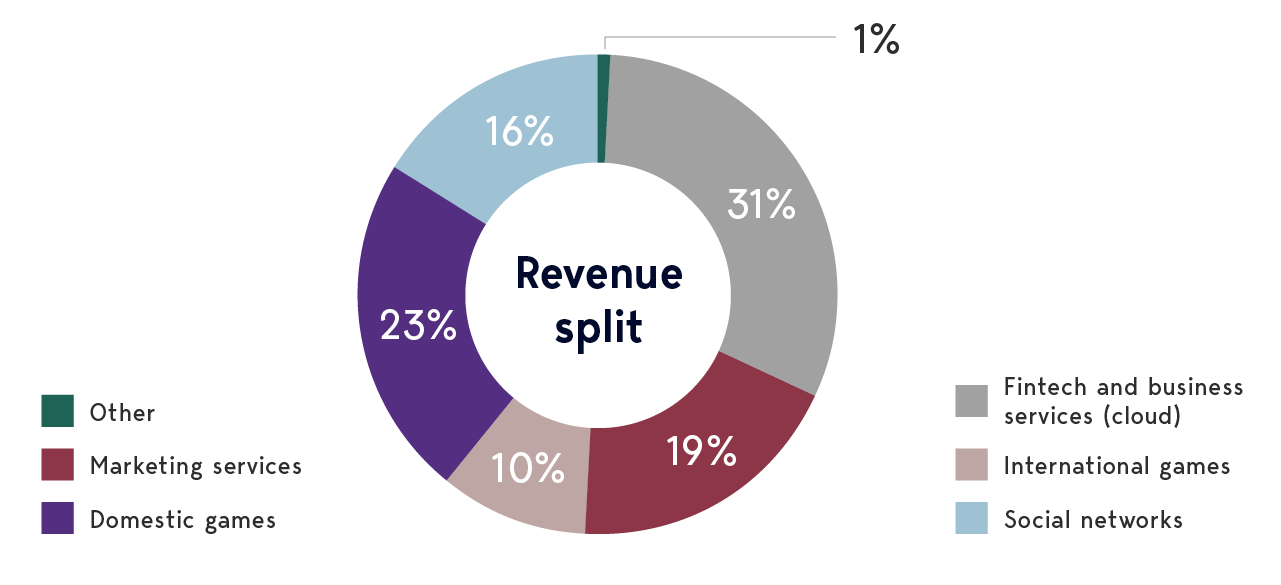

Games, payments and everything

Tencent has a deep bench of growth drivers

Source: Tencent earnings presentation Q1 2026

One app to rule them all

Founded in Shenzhen in 1998, Tencent started life with a focus on instant messaging, its QQ platform quickly becoming the default option for a generation of early internet adopters. Gaming, payment and content functions soon followed, before the transformational release of the messaging service Weixin – known as WeChat outside China – in 2011.

Whereas QQ was rooted in the desktop era, Weixin was designed for the mobile age. Rapid innovation, notably Weixin Pay in 2013 and Mini Programs in 2017, drove an unprecedented level of integration, establishing the template for the modern “super app”. Users can communicate, consume content, play games, access services, shop and make payments without ever having to leave Weixin.

Today, Weixin is an indispensable part of daily life for more than one billion Chinese. It is, in effect, the default operating system for mobile consumers and commerce. In the world’s largest internet market, this ubiquity provides a strong position from which to drive growth.

The scale of Weixin and Tencent’s wider ecosystem forms a formidable competitive moat that entrenches leadership across much of China’s digital economy. This reach fuels a classic flywheel: a vast user base draws in merchants and developers, which in turn enhances the platform’s appeal. The resulting self-reinforcing dynamic has supported consistent revenue growth and a highly profitable, cash generative business model, all underpinned by a rock-solid balance sheet.

Diversified growth engines

This strong financial profile has enabled Tencent to reinvest in growth, consolidate market share and pursue new avenues of expansion. In turn, the company benefits from a diversified set of growth drivers, each reinforced by powerful network effects.

Gaming

Gaming is Tencent’s core cash generator. Through a portfolio of leading titles, such as Honour of Kings, Peacekeeper Elite, Delta Force and Clash of Clans, the company commands an estimated 45% share of the domestic market.

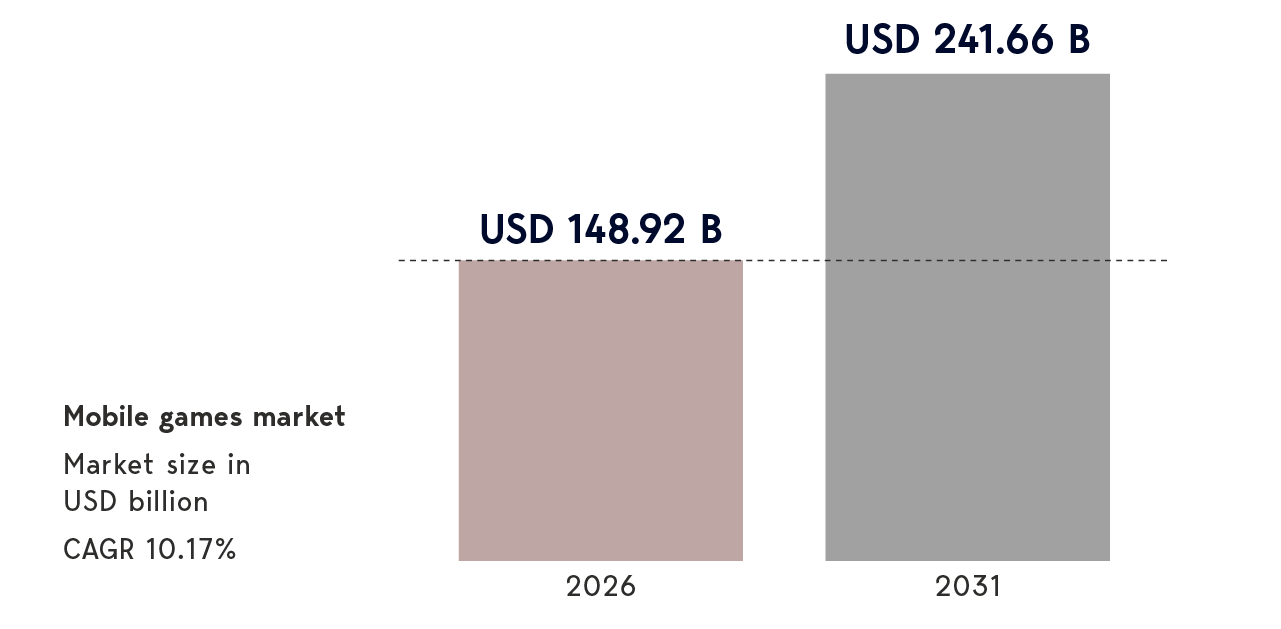

Internationally, Tencent’s presence is more modest, although franchises like Clash of Clans and PUBG Mobile are driving market share gains. The company’s focus on free-to-play mobile gaming – where revenues are driven by in-game purchases – aligns well with prevailing market dynamics. Mobile gaming is now bigger in revenue terms than PC and console gaming combined.

Going mobile

Mobile gaming is growing strongly

Source: Mordor Intelligence, January 2026

Advertising

Weixin offers a compelling value proposition to advertisers. Extensive user data and engagement facilitates precise targeting and measurable returns. Historically, Tencent has been conservative in how many ads it shows customers, preferring to strengthen its position with users by keeping the “ad-load” – the amount of advertising shown relative to content – deliberately low. This leaves ample scope to increase advertising and, with it, monetisation.

Fintech

WeixinPay is one of two dominant payment services in China. Most revenue is driven by fees on over one billion daily transactions, combined with withdrawal and credit card repayment charges. Leveraging its huge user base, Tencent also distributes banking and wealth management services, and consumer loans.

The future of growth

Looking ahead, however, the trajectory and durability of Tencent’s growth engines will be increasingly shaped by AI. Just as Weixin underpinned the transition from desktop to mobile, the next phase of growth will hinge to a large degree on the company’s ability to successfully embed AI across its ecosystem.

Until recently, many investors viewed Tencent as something of an AI laggard, particularly when set against the more vocal ambitions of domestic peers like Alibaba and ByteDance. Where others sought early prominence, Tencent prioritised the steady development of foundational capabilities. Proprietary AI inference chip Zixiao was launched in 2021, with large language model Hunyuan following in 2023.

The emphasis has now turned firmly towards commercialisation, with investment ramping up and AI more visibly deployed across platforms. Weixin provides a vast distribution network through which AI can be seamlessly integrated into everyday activities. This is particularly powerful in the case of Mini Programs; millions of embedded, lightweight apps that allow users to access services and perform tasks without leaving Weixin.

Progress is not confined to consumer-facing applications; it increasingly extends into enterprise settings, where the potential for long-term monetisation may ultimately prove more compelling. Agentic tools are gaining traction, signifying AI’s transition from passive chatbot to active workplace assistant. Tencent’s WorkBuddy, for example, is believed to be the most widely used agentic productivity tool in China.

If past is prologue, Tencent appears well equipped to navigate the transition to AI. Under founder and CEO Pony Ma, the company has repeatedly demonstrated an ability to adapt through periods of profound technological and political change – from the shift from desktop to mobile, to the regulatory reset in China in 2021 and 2022.

Such episodes are rarely straightforward, yet Tencent has tended to emerge in a stronger position. Disruption has, in practice, validated the resilience of a model defined by powerful network effects, market leadership and enduring competitive advantages. The AI revolution is unlikely to be different.

Important Information

This article is provided for general information only and should not be construed as investment advice or a recommendation. This information does not represent and must not be construed as an offer or a solicitation of an offer to buy or sell securities, commodities and/or any other financial instruments or products. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorised.

Stock Examples

The information provided in this article relating to stock examples should not be considered a recommendation to buy or sell any particular security. Any examples discussed are given in the context of the theme being explored.