Putting a Price on Carbon

The concept of carbon pricing has been around for some time. However, as climate concerns have moved steadily up the political agenda in recent years, calls to put a price on carbon and charge polluters for emissions have intensified.

In 1920, the economist Arthur Cecil Pigou considered the concept of ‘externalities’ in his work “The Economics of Welfare”. Defined as the costs or benefits of an economic activity experienced by an unrelated third party, Pigou believed market forces could not always effectively address externalities and that corrective intervention was often justified. The idea of Pigouvian taxes was born. In the present day, no externality generates as much discussion as climate change and many propose carbon pricing as a necessary corrective.

How does carbon pricing work?

Broadly speaking, there are two forms of carbon pricing in operation around the world today: carbon taxing and emissions trading systems (ETS). Under a carbon tax regime, the regulating authority directly sets the price of carbon. The benefit of a carbon tax is that it fixes the price of carbon, although it offers no guarantees around the level of emissions. An ETS, meanwhile, sets a cap on the total amount of greenhouse-gas emissions (GHG) in a year. Here, the level of emissions is fixed, but there are no guarantees around the cost of doing so.

Advantages and Disadvantages of Carbon Pricing

“There is a growing consensus that carbon pricing—charging for the carbon content of fossil fuels or their emissions—is the single most effective mitigation instrument.” Christine Lagarde, Managing Director of the International Monetary Fund, and Vitor Gaspar, Director of the International Monetary Fund’s Fiscal Affairs Department.

Most observers consider carbon prices to be a cost-effective policy for tackling climate change for three key reasons:

- They incentivise polluters to reduce emissions as long as it is cheaper than paying the penalty.

- They decentralise emission-reduction decisions − government does not need to stipulate how polluters should reduce emissions, only that they should.

- They encourage innovation.

There are criticisms too, however, such as the potential outsized financial impact on low-income households. Assessing the effectiveness of such schemes is also problematic, given success is measured against an uncertain counterfactual reference point − what would have happened if the scheme had not been introduced? Compounding these issues is widespread political and public opposition, perhaps best exemplified by Australia’s decision to repeal its carbon tax in 2014. So while the advantages of carbon-pricing schemes may appear self-evident, the decision to introduce one is not risk free for policymakers.

Carbon pricing today

Source: World Bank – Carbon Pricing Dashboard 2020

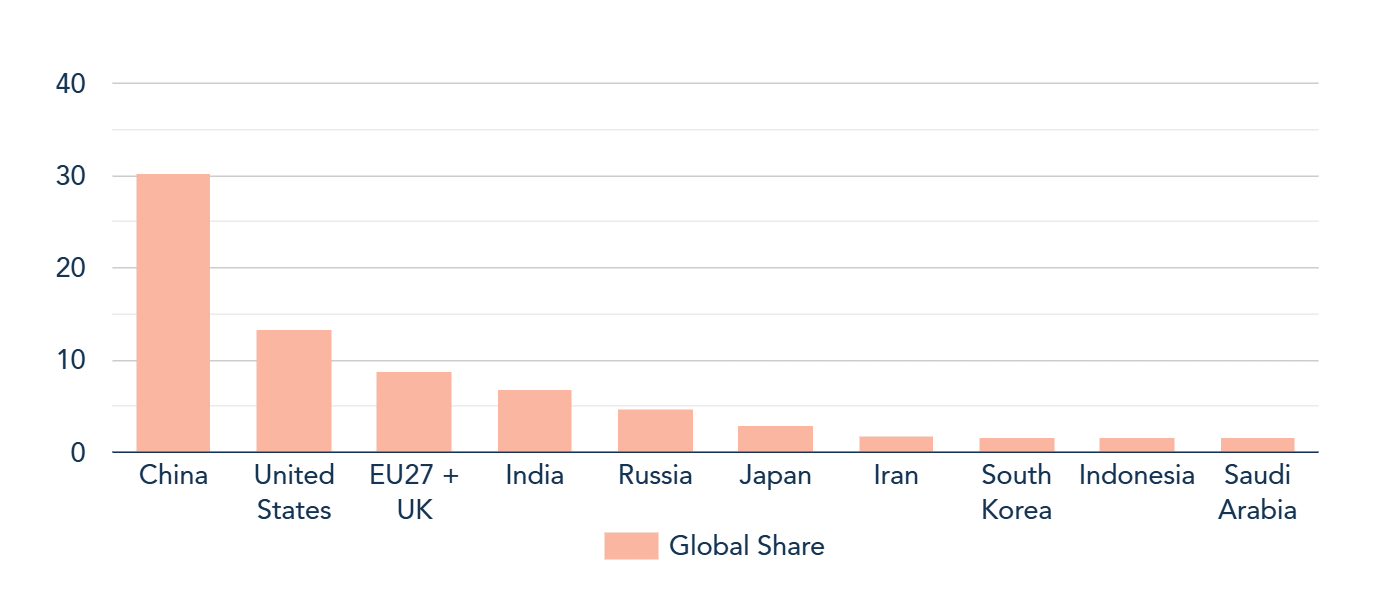

For carbon pricing to really make a difference depends on action by the world’s three biggest polluters; China, the US and the European Union, together responsible for around 50% of global CO2 emissions in 2019.

Top emitting countries by global share (%)

Source: European Commission JRC Science for Policy Report, Fossil CO2 emissions of all world countries 2020.

The EU currently has a carbon-pricing scheme in place covering its full jurisdiction, while China recently implemented a nationwide ETS, having run pilot schemes in seven major cities prior to doing so. Progress is less apparent at the federal level in the US, although certain states, particularly California, have programmes in place. However, President Biden has signalled his support for a federal scheme for the utility sector. As such, while adoption remains patchy, the overall direction of travel appears to be towards the use of carbon pricing as a key policy instrument in mitigating global emissions.

While proponents of carbon pricing will welcome this trend towards greater adoption, in its current guise it is by no means a silver bullet. One glaring deficiency is the price most schemes put on carbon. Of the global emissions currently covered by a scheme, less than 5% are priced at a level consistent with a cost-effective delivery of the Paris agreement’s emission-reduction goals1.

Many companies and organisations are not waiting for government and regulators to price their carbon emissions for them. Internal carbon pricing has become increasingly common in recent years as companies integrate climate risks and opportunities into their long-term business strategies. So far, around 1,700 global companies have adopted internal carbon pricing or plan to implement a scheme within two years2.

Companies’ Objectives for Implementing an Internal Carbon Price

Source: State and Trends of Carbon Pricing. World Bank Group, May 2020

At present, there are three distinct approaches to internal carbon pricing: an internal carbon fee, a shadow price and an implicit price. In reality, many companies use a hybrid model of all three.

- Internal Carbon Fee

An internal carbon fee places a monetary value on each tonne of carbon dioxide, which is readily understandable throughout the business. This is an internal carbon tax charged to business units for their emissions. Companies will then use the revenue generated from the carbon fee to fund GHG-emission-reduction measures, renewable-energy purchases and carbon offset projects. Evidence suggests that where internal carbon fees are in place they are typically set at a relatively low level to avoid overburdening business units. - Shadow Price

A shadow price is a theoretical carbon price aimed at supporting long-term business planning and strategy. It is the most commonly adopted form of internal carbon pricing. As it is only a theoretical price, however, a shadow price collects no revenue. What it does do is allow companies to evaluate investments and test assumptions in the anticipation of future carbon constraints, and shift investment towards projects that would be competitive in a carbon-constrained world. Many companies apply a shadow price above current government levels to prepare for a future of more stringent regulatory constraints. This can be helpful in determining whether long-lived capital assets face the risk of becoming stranded assets. - Implicit Price

A company will base an implicit carbon price on how much it spends to reduce its GHG emissions in order to comply with government regulations. This implicit price enables a company to identify the main costs required to reduce its carbon footprint. The information gleaned from an implicit carbon price can allow the company to initiate a carbon-pricing programme that uses internal carbon fees and shadow prices.

Microsoft Corporation is an example of a company embracing internal carbon pricing as it takes steps to address it carbon emissions. In 2020, the company announced an ambitious plan to be carbon negative by 2030 and, by 2050, to have removed from the environment all the carbon it has emitted since the business was founded in 1975. Integral to the plan is the extension of the company’s existing internal carbon fee (introduced in 2012 and presently covering scope 1 and 2 emissions) to cover scope 3 emissions. While priced a lower price per tonne than the current $15 charged on scope 1 and 2 emissions, over time this will increase until the same internal fee applies to all emissions. Importantly, this is not a shadow fee; every business division at Microsoft has to pay for its scope 3 emissions, thereby incentivising emission reduction and funding further carbon removal investment.

Likewise, in 2016 Unilever moved from shadow pricing to a scheme whereby each of its business divisions has internally priced emissions from its manufacturing operations subtracted from capital budgets at the start of the year. All money raised goes into a central clean technology fund, which business divisions can access by bidding for projects that meet Unilever’s emissions-reducing criteria. The company has credited the scheme with encouraging employees to explore and embrace previously unknown technologies.

Microsoft and Unilever are just two examples of the drive among corporates to limit their carbon footprint by the use of carbon pricing. When set at an appropriate level, such schemes can be an effective and flexible tool in facilitating the transition to a lower-carbon operating model and supporting innovation and investment in newer, more efficient technologies and industries. We expect this trend to continue, and for carbon pricing and the concomitant financial implications to become increasingly important considerations when making long-term investment assumptions. Adapt and reduce carbon emissions and companies are likely to be rewarded, fail to keep up and companies will have to bear the considerable costs of higher carbon prices and the risks that poses to existing business models.

- State and Trends of Carbon Pricing. World Bank Group, May 2020

- State and Trends of Carbon Pricing. World Bank Group, May 2020

Important Information

This article is provided for general information only and should not be construed as investment advice or a recommendation. This information does not represent and must not be construed as an offer or a solicitation of an offer to buy or sell securities, commodities and/or any other financial instruments or products. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorised.

Stock Examples

The information provided in this article relating to stock examples should not be considered a recommendation to buy or sell any particular security. Any examples discussed are given in the context of the theme being explored.